Home » PSApedia

Value-at-risk

Empower your financial strategy with precision using our Value-at-Risk solutions.

What Is Value-at-Risk?

Value-at-Risk (VaR) serves as a quantitative measure used to estimate the potential loss in value of a portfolio or investment within a specific timeframe and confidence level. It is a widely used risk management tool in finance to assess and manage potential financial risks.

In Professional Service Automation (PSA), Value-at-Risk (VaR) is a statistical technique used to measure and quantify the level of financial risk within a firm over a specific time frame. It estimates the maximum potential loss that might be experienced under normal market conditions.

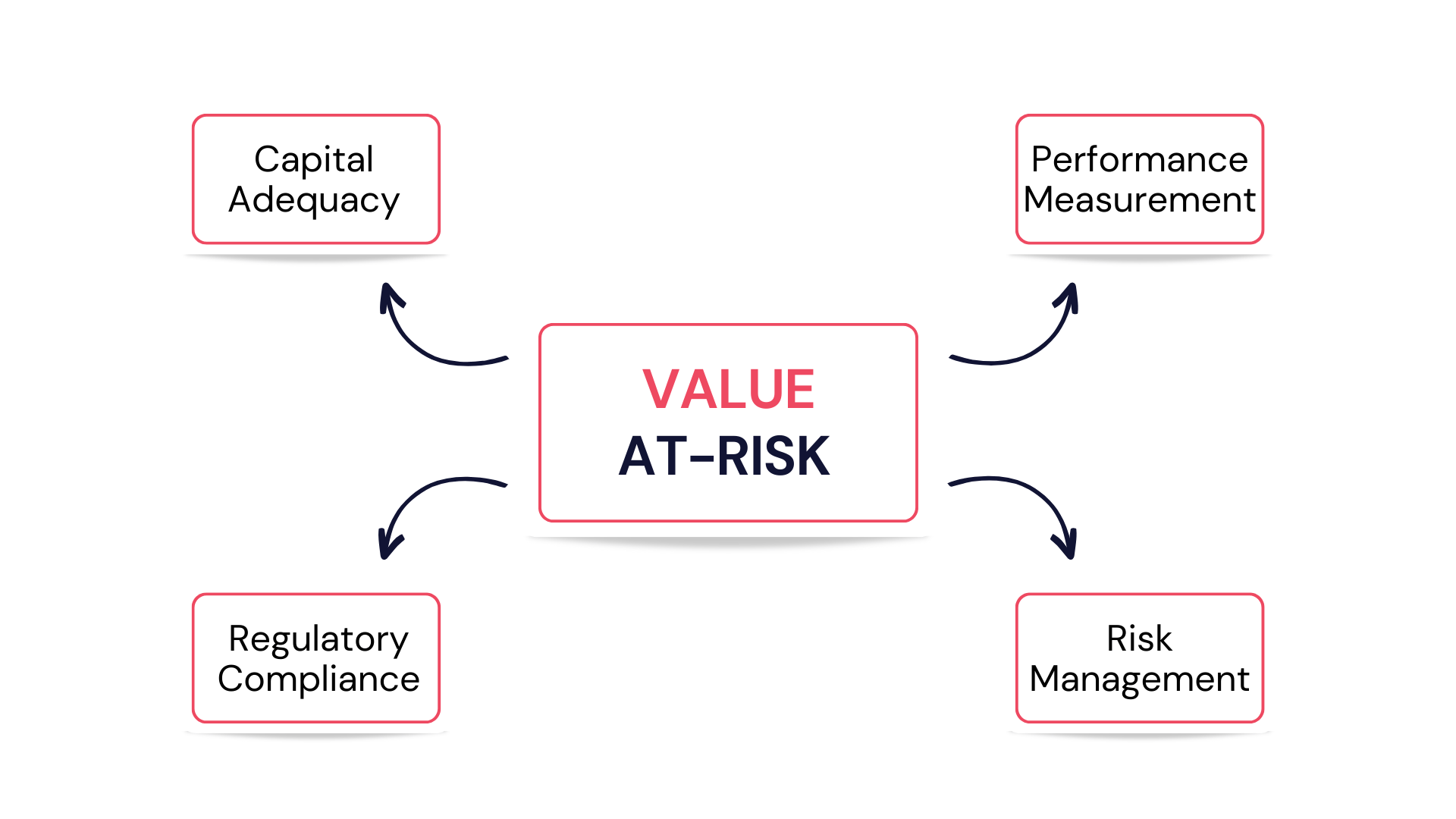

Significance of VaR

VaR holds significant importance in risk management as it provides a numerical estimate of the maximum potential loss that an investment or portfolio might face. This metric aids in setting risk tolerance levels, making informed investment decisions, and ensuring financial stability.

1. Risk Quantification: VaR provides a quantifiable measure of financial risk, facilitating informed decision-making.

2. Resource Allocation: Helps in allocating resources effectively by identifying potential financial vulnerabilities.

3. Compliance and Reporting: VaR is often used to comply with financial regulations and for reporting to stakeholders.

Significance of VaR

How to calculate Significance of VaR?

VaR is typically calculated using statistical models that consider the probability and magnitude of potential losses. The calculations might involve historical data, variance-covariance models, or Monte Carlo simulations.

VaR can be calculated using various methods, with the most common being the historical method and the variance-covariance method. The formula for the variance-covariance method for a specified confidence level is:

VaR = Z × σ2 × P × T

- Z represents the Z-score or the number of standard deviations corresponding to the desired confidence level.

- σ denotes the standard deviation of the portfolio’s returns.

- P signifies the portfolio value.

- T stands for the time horizon.

Example of Value-at-Risk (VaR) Calculation

Suppose an investment portfolio with a value of $1,000,000 has a standard deviation of returns of 0.02 and a one-day time horizon. To calculate the VaR at a 95% confidence level (corresponding to a Z-score of 1.645):

VaR==1.645×0.022×1,000,000×1

=32,900

Thus, the Value-at-Risk for this investment portfolio at a 95% confidence level is $32,900.

VaR Compared to Other Risk Assessment Metrics

In comparison to risk measurements such as standard deviation or beta, VaR provides a particular calculation of prospective losses at a given confidence level over a specified time period. It aids in recognizing the downside risk of an investment or portfolio.

1. Stress Testing: Unlike stress testing, which evaluates potential losses under extreme market conditions, VaR focuses on losses under normal market conditions.

2. Expected Shortfall: Expected shortfall considers the size of losses in the worst-case scenarios, whereas VaR sets a threshold for the maximum expected loss.

| Risk Metric | Definition | Importance / Use |

|---|---|---|

| Value-at-Risk (VaR) | Estimation of potential loss in value within a specified horizon | Measures the potential financial loss at a given confidence level |

| Risk-adjusted Return on Capital (RAROC) | Ratio of return to risk exposure adjusted for risk | Indicates the return generated per unit of risk in a project or investment |

| Risk Exposure | Extent of potential loss or harm to an organization | Evaluates the overall exposure to potential risks and their impact |

| Risk Mitigation Strategies | Actions taken to minimize or manage potential risks | Reflects the measures and strategies implemented to reduce risk exposure |

Best Practices for Managing VaR in PSA

VaR analysis aids financial institutions, fund managers, and investors in setting risk management strategies, determining capital requirements, and evaluating the potential impact of adverse market movements on their portfolios.

1. Regular Monitoring: Continuously monitoring and updating VaR calculations to reflect current market conditions and the firm’s financial position.

2. Diversification: Diversifying investments and projects to mitigate potential risks identified by VaR analysis.

3. Data Analysis: Employing robust data analytics, such as those provided by KEBS, for accurate risk assessment and management.

Ready to Optimize Your Risk Management?

KEBS offers comprehensive financial risk management tools and solutions that assist in assessing and managing Value-at-Risk within investment portfolios. By utilizing KEBS functionalities, businesses can effectively monitor and mitigate potential financial risks.

Utilizing KEBS analytics capabilities to analyze financial data and assess risk profiles. Managing financials effectively with KEBS comprehensive software, aiding in risk quantification and control. Generating detailed reports to monitor VaR and other financial risks, using KEBS custom reporting tools.

KEBS Finance Management

To learn more about integrating effective VaR management in your PSA operations with KEBS, contact us or request a demo.