What Is Budget vs Actual Variance?

Budget vs. actual variance analysis is a vital tool for financial management and decision-making. Businesses employ it to evaluate their financial performance by comparing planned budgets to actual results.

This analysis finds what went well and what didn’t, helping organizations adjust strategies, use resources better, and keep getting better financially. By pinpointing discrepancies between expectations and reality, companies can make informed decisions, enhance profitability, and steer toward achieving their financial goals.

Budget vs. Actual Variance is a tool business uses to compare planned figures with real outcomes for financial analysis. It’s like a mirror for money, showing how a company is doing compared to its plans at this time. Comparing planned costs and revenues to actual ones indicates a company’s financial performance. It highlights areas where the company is exceeding or falling short of expectations.

Why is Budget vs Actual Variance Important?

The power of budget vs. actual variance lies in its simplicity. It serves as a financial compass, guiding businesses in the right direction. By comparing planned and actual spendings or earnings, businesses can identify financial strengths and weaknesses, spot trends, and make informed decisions.

Let’s say your actual costs are higher than budgeted. It might be because of unexpected expenses, inefficiencies, or price increases. Conversely, if your actual revenues are lower than budgeted, it may result from lower sales, pricing issues, or market changes. Budget vs. actual variance analysis brings these anomalies to light, enabling strategic adjustments.

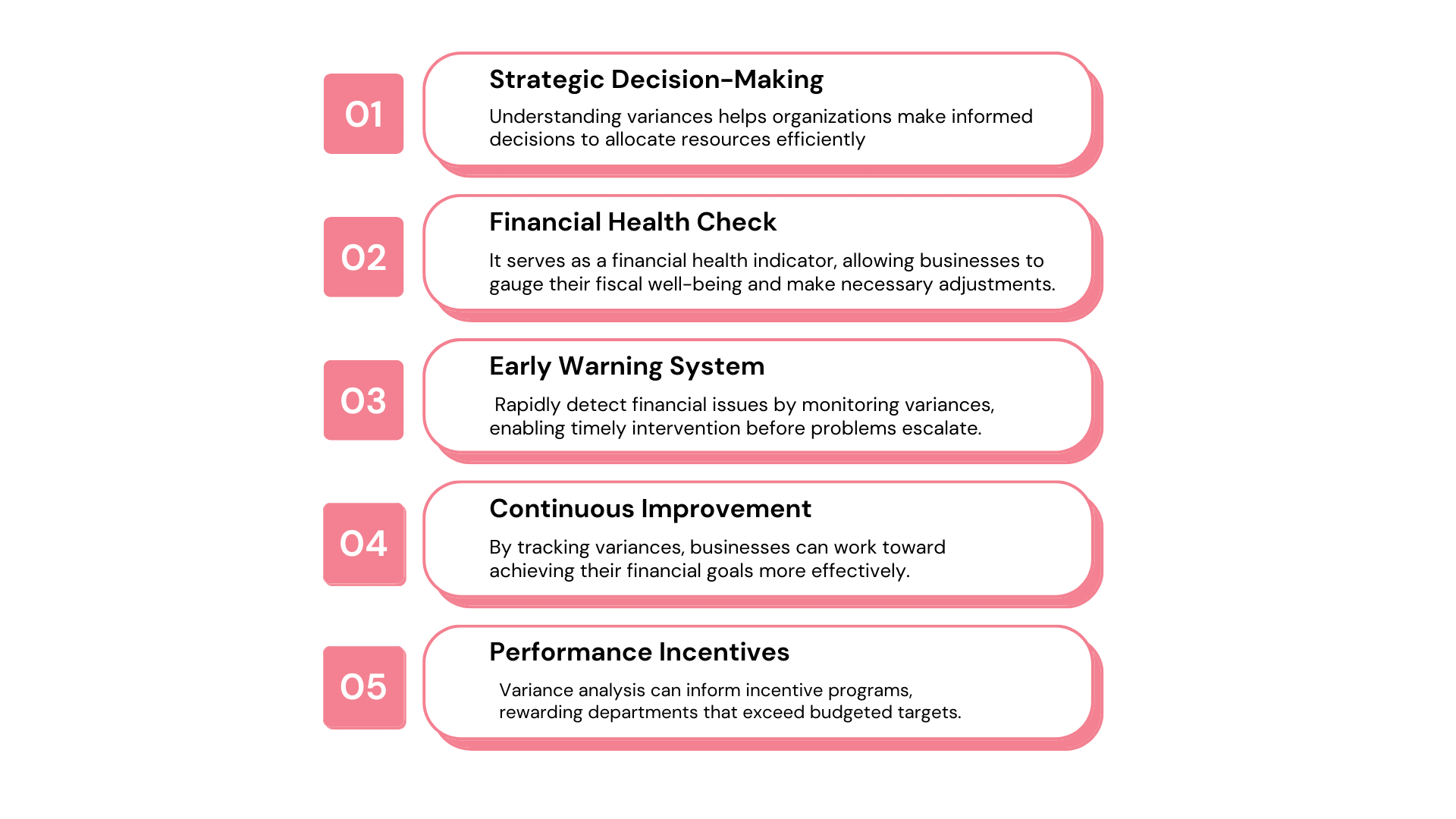

Features of Budget vs Actual variance

How to Calculate Budget vs Actual Variance: Formula and Example

To calculate the budget vs. actual variance, you need to compare the actual financial results with the budgeted or planned figures. The formula for calculating the budget vs. actual variance is

Budget Variance = Actual Amount – Budgeted Amount

Positive variance indicates that actual revenues are higher, or costs are lower than the budget, signaling good performance. Negative variance indicates the opposite.

Let’s illustrate this with an example. Suppose you budgeted $10,000 for marketing in Q3.

However, actual expenses came to $12,000. The budget variance is $12,000 – $10,000 = -$2,000. This negative variance indicates you’ve overspent on marketing.

The Difference Between Budget Variance and Forecast Variance

While both budget variance and forecast variance assess financial performance, they serve different purposes.

Budget variance, as we’ve discussed, compares budgeted figures with actual results. Forecast variance, on the other hand, compares forecasted figures—updated predictions based on current conditions—with actual outcomes. While budget variance helps assess the initial plan’s accuracy, forecast variance aids in understanding the accuracy of updated predictions.

How is Budget vs Actual Variance Used?

Budget vs. Actual Variance is a strategic tool. It offers valuable insights that can aid in financial planning, cost control, performance evaluation, and strategic decision-making.

Budget variance measures the gap between actual financial results and the established budget, offering a retrospective view. It helps identify where plans exceeded or fell short. In contrast, forecast variance compares actual results to the latest forecasts, giving a forward-looking perspective to refine future predictions.

For instance, a consistent positive variance in revenues might suggest that the sales team is performing exceptionally well. Conversely, a recurring negative variance in a specific cost area might pinpoint inefficiencies that need addressing.

Budget vs. Actual Variance vs Profit

Budget vs. actual variance is a crucial financial metric that helps businesses assess their financial performance. It compares the expected budgeted figures with the actual results achieved, highlighting areas where the company exceeded or fell short of its financial goals. Positive variances indicate that a company performed better than expected, while negative variances signal potential financial challenges. Analyzing these variances enables companies to make informed decisions, adjust strategies, and allocate resources more effectively to optimize profitability.

Profit, on the other hand, represents the ultimate goal of any business endeavor. It’s the positive difference between revenue and expenses, indicating the company’s financial success or failure. When budget vs. actual variance analysis reveals positive variances, it often translates into higher profits, reflecting efficient operations and sound financial management.

Conversely, negative variances may lead to reduced profits, prompting businesses to identify cost-saving measures or revenue-boosting strategies to improve their bottom line. In essence, monitoring budget vs. actual variance is a critical step in achieving and sustaining profitability in the dynamic world of business.

| Aspect | Budget | Actual Variance | Profit |

| Definition | Planned financial expectations for a specific period. | The difference between the budgeted amount and the actual amount spent or earned. | The net earnings after deducting expenses from revenue. |

| Purpose | To set financial targets and allocate resources. | To assess the variance between planned and actual financial performance. | To measure the overall financial success or loss of a business. |

| Time Frame | Forward-looking, covering a future period. | Backward-looking, analyzing past performance. | Typically covers a specific period, like a fiscal year. |

| Focus | Planning and forecasting. | Evaluation of performance against the budget. | Overall financial health and sustainability. |

| Calculation | Prepared based on estimates and assumptions. | Calculated by subtracting actual figures from budgeted figures. | Calculated by deducting expenses from revenue. |

Optimize Your Financial Management with KEBS

Ready to streamline your financial management? With KEBS, a leading PSA software, you can efficiently manage your budgeting, track actual spending, and calculate variances effortlessly. By integrating financial data and providing real-time insights, KEBS empowers businesses to enhance financial performance and make strategic decisions. Dive into the world of smart budgeting with KEBS today!

KEBS Implementation

Explore the KEBS Demo today. If you have any questions, need assistance, or want to get in touch with KEBS, don’t hesitate to contact us.