Home » PSApedia

Accounts Receivable Turnover

Optimize Your Finances and improve Cash Flow with High Accounts Receivable Turnover.

What is Accounts Receivable Turnover?

Accounts Receivable Turnover is a financial metric that measures how efficiently a business collects its owed debts from customers. Essentially, it evaluates the frequency at which a company turns its receivables into cash within a specific period.

Every business aims to sell, and many of these sales occur on credit. But selling is just half the task – collecting payment is equally vital. This is where Accounts Receivable Turnover (ART) plays its part. ART, a financial metric, gives insights into a company’s ability to collect owed money.

The Mechanics Behind Accounts Receivable

Before diving into ART, it’s essential to understand accounts receivable itself. Whenever a company makes a sale and doesn’t receive payment immediately, it records the owed amount under accounts receivable. It signifies a short-term obligation from the customer to the company.

For efficient business operations, especially for those in the PSA sector, tracking and understanding these credits is pivotal. Delve into the intricacies of the PSA sector to gain a better grasp.

Why is Accounts Receivable Turnover Important?

ART isn’t just a fancy term; it’s the backbone of a company’s financial health. A high turnover rate indicates that a business is efficient in its collections, leading to consistent cash flow. A low rate could mean issues with collecting money or customers not being able to pay back their debts.

Companies can use this measure to evaluate their financial health. They can also improve their cash flow and make sure that they do not unnecessarily tie up money in unpaid earnings. In the vast realm of finance, metrics like these can be invaluable for businesses.

Importance of Accounts Receivable Turnover

Calculating Accounts Receivable Turnover

ART= Net Credit Sales / Average Accounts Receivable

Detailed Example: Consider Company X, operating in the PSA sector, with net credit sales of $2 million over a year. The beginning receivables were $200,000, and ending receivables were $250,000.

Average Accounts Receivable = (Beginning + Ending Receivables)/2

= (200,000+250,000)/2 = $225,000

ART=2,000,000/225,000 =8.89

This means Company X collects its outstanding credits almost 9 times a year.

Accounts Receivable Turnover vs. Cash Conversion Cycle

While ART focuses on collections, the Cash Conversion Cycle (CCC) looks at the entire process – from buying inventory to collecting cash for it. In many financial analyses, both metrics are used in tandem to gauge overall efficiency.

| Metric | Definition | Example |

|---|---|---|

| Accounts Receivable Turnover | This measures how effectively a company is collecting its receivables. It is calculated as: Net Credit Sales / Average Accounts Receivable | If a company has Net Credit Sales of $1,000,000 and Average Accounts Receivable of $250,000, then its Accounts Receivable Turnover is 4 times per year. This means the company collects its average receivable 4 times a year. |

| Cash Conversion Cycle | This measures how long it takes a company to convert its investments in inventory and other resources into cash flows from sales. It is calculated as:

Days Inventory Outstanding + Days Sales Outstanding – Days Payable Outstanding |

If a company has Days Inventory Outstanding of 30 days, Days Sales Outstanding of 40 days, and Days Payable Outstanding of 20 days, its Cash Conversion Cycle is 50 days.

This means it takes 50 days for the company to see a return on its investment. |

Using Accounts Receivable Turnover in Financial Analysis

ART isn’t a standalone metric; it’s part of a bigger financial picture. Comparing your ART with industry benchmarks can be insightful. And with detailed financial strategies, it’s possible to pinpoint inefficiencies and rectify them.

The ratio shows how many times a business can convert its receivables into cash. It does this by comparing net credit sales to average accounts receivable. A higher turnover rate suggests that the company collects its receivables quickly, indicating good credit management practices. Conversely, a lower rate might signal potential collection issues or a lenient credit policy. Thus, for analysts and investors, understanding this ratio can provide a clearer picture of a company’s financial health and operational efficiency. Several factors can influence your ART:

- Credit Policy: If your terms are too lenient, collections might delay.

- Industry Standards: Some industries naturally have higher ART due to their nature.

- Economic Conditions: During downturns, collections might slow down.

- Internal Practices: Inefficient invoicing and follow-up can also affect your ART.

The Role of KEBS in Accounts Receivable Management

With technology driving modern businesses, PSA software like KEBS has become indispensable. It streamlines invoicing, monitors receivables, predicts collections, and provides actionable insights. Keen on optimizing your receivables management? Check out how KEBS can help.

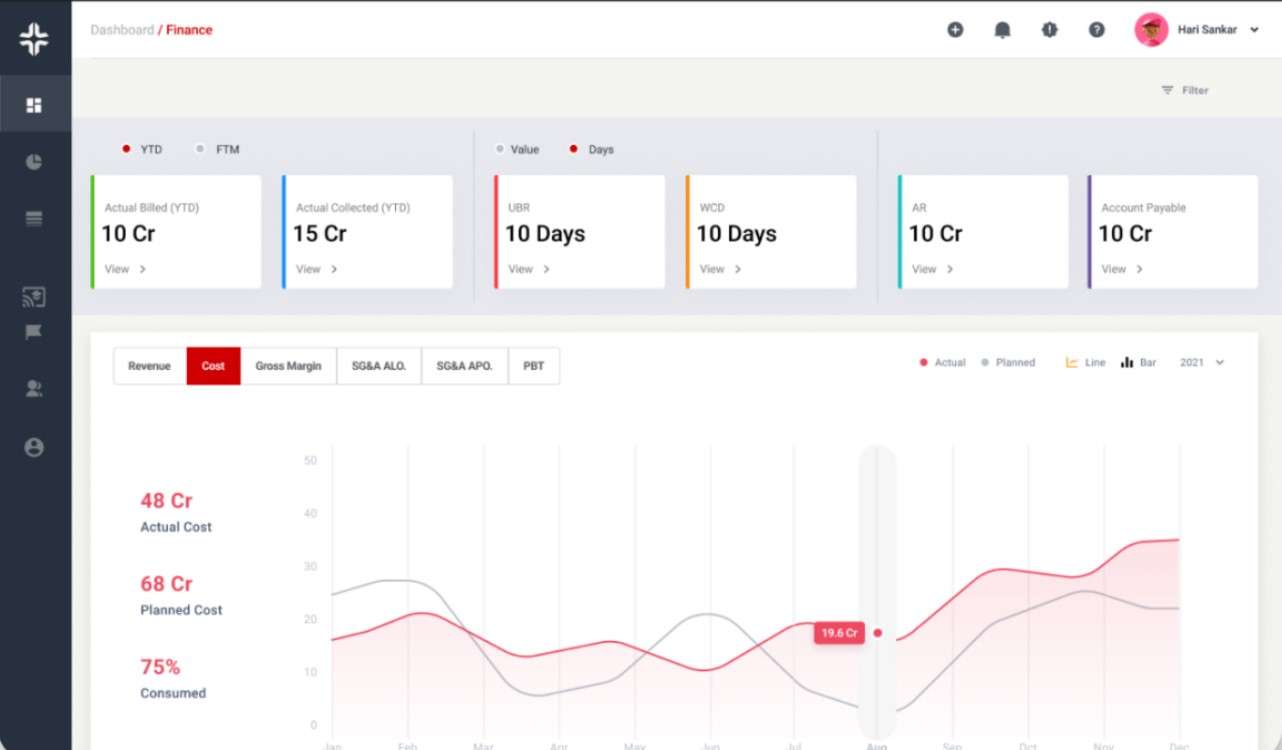

KEBS Finance Management

Maintaining a favorable ART is vital for any business, ensuring liquidity and operational efficiency. With tools like KEBS, managing ART and other financial metrics has never been easier. Ready to optimize your ART with KEBS? Contact us today or schedule a demo.